Sat 7-7-18 Big Pic: AII: The American Association of Individual Investors

A Quantitative Method for Asset Allocation

by Joseph Harding

Article Highlights

· Conventional rebalancing readjusts the portfolio back to the

predetermined target allocation for stocks.

· The quantitative method considers not only the target allocation

but also the prevailing valuation of stocks and the relative valuation of

bonds.

· Returns are enhanced for portfolios holding allocations of 50%,

60% and 70% to stocks; volatility is reduced for equity allocations up to 90%.

An

individual investor must decide how to allocate portions of their portfolio

among different asset classes, such as stocks, bonds or cash. A diversified

portfolio allocated among different asset classes has been proven to be an

excellent strategy for obtaining good returns over the long term, with the

added benefit of reduced volatility (i.e., avoiding large changes in portfolio

value) over the short term.

|

TAKE A PEEK

at all the member benefits AAII has to AAII is a nonprofit association dedicated to investment education. |

Indeed, AAII conducts an ongoing Asset Allocation Survey , with results

updated every month (www.aaii.com/assetallocationsurvey).

The survey measures the percentage holdings of members in five asset

categories: stock funds, stocks, bond funds, bonds and cash.

Conventional

Method for Asset Allocation

So how

does an investor go about determining the appropriate asset allocation for

their portfolio? There are two generally accepted guidelines for making this

determination.

The first guideline is that an investor must determine their

tolerance for risk. In other words, how willing are you to endure large swings

in portfolio value over the short term in exchange for potentially higher returns

over the long term? If you determine that you are willing to endure large

swings in portfolio value over the short term, then a higher percentage of

stocks compared to bonds or cash in your portfolio would be appropriate. If, on

the other hand, you determine that you are not as willing to endure large

swings in portfolio value over the short term, then a lower percentage of

stocks compared to bonds or cash in your portfolio would be appropriate.

The

second guideline is based on the expected retirement date of the investor. An

investor who is many years away from retirement should have a higher allocation

to stocks compared to bonds or cash. However, an investor who is either retired

or is only a few years away from retirement should have a lower allocation to

stocks compared to bonds or cash. Indeed, this is the idea behind the various

target date funds that are available today.

After

determining the appropriate asset allocation for your portfolio, it is not wise

to simply “set it and forget it.” Over time, the value of one asset class will

likely change compared to other asset classes. This means that over time, the

asset allocation of your portfolio will also change compared to your original

target allocation. Therefore, it is recommended that an investor should rebalance

their portfolio at least annually. During the rebalancing process, portions of

portfolio assets that have increased in relative value are sold, with the

proceeds invested in assets that have decreased in relative value. The result

is that the portfolio is readjusted back to the original target allocation

after the rebalancing is completed.

The

Quantitative Method

{kind=link}

The

conventional method for asset allocation described so far has been proven over

time to be a good model for individual investors to follow. But what if there

is a better way?

When an

investor rebalances their portfolio, what if the investor adjusts their actual

target allocation after rebalancing based on not only their target allocation

but also the current prevailing relative value of the stock and bond market?

In the

quantitative method described herein, the allocation to stocks would be equal

to the investor’s target allocation if the current prevailing valuation of the

stock market is historically average compared to the current prevailing 10-year

Treasury note yield. However, the allocation to stocks would be greater than

the investor’s target allocation if the current prevailing valuation of the

stock market is historically below average compared to the current prevailing

10-year Treasury note yield. The allocation to stocks would be less than the

investor’s target allocation if the prevailing current valuation of the stock

market is historically above average compared to the current prevailing 10-year

Treasury note yield.

Stock Market

Valuation

A well-known method for determining the valuation of the U.S.

stock market (specifically the S&P 500 index) is the cyclically adjusted

price-earnings ratio, or CAPE ratio. This ratio, invented by Robert Shiller of

Yale University, compares the current level of the S&P 500 to its average

earnings over the last 10 years, adjusted for inflation. A high CAPE value

indicates that the stock market is overvalued, while a low CAPE ratio indicates

that the stock market is undervalued. A spreadsheet that includes all of the

relevant data for calculating CAPE is publicly available at www.econ.yale.edu/~shiller/data.htm.

The quantitative method for asset allocation described here is

based on the data contained in this spreadsheet but does not use the calculated

CAPE Shiller from the spreadsheet directly. Instead, the quantitative method

uses a 20-year period of earnings for calculating CAPE (denoted as CAPE20) and

also takes into account the current S&P 500

dividend yield compared to the current 10-year Treasury note yield.

Taking

the S&P 500 dividend yield and the 10-year Treasury note yield into account

makes logical sense. Low bond yields compared to their historical average (as

has been the case for the last several years) should support a stock market

with a higher than average CAPE. The opposite should be true if bond yields are

high compared to their historical average.

Quantitative

Method Formula

The

following formula is used in the quantitative method for determining the actual

allocation to stocks during rebalancing:

Stock

allocation = [target stock allocation + (2 × CAPE avg) – (2 × CAPE20)] × K

Where:

· Stock allocation is the actual stock allocation used by the

investor during rebalancing, in percent;

· Target stock allocation is the investor’s target allocation

to stocks;

· CAPE avg is the average value of CAPE20 over the last 600

months (50 years);

· CAPE20 is the cyclically adjusted price-earnings ratio over

the last 20 years; and

· K is 1.5 × (S&P 500 dividend yield ÷ 10-year Treasury

note yield).

The CAPE20 uses 20 years of earnings versus the 10 years of

earnings used in Shiller’s CAPE ratio. The S&P 500 yield can be calculated

using data from Shiller’s spreadsheet; simply divide the dividend by the

S&P 500 composite value. The 10-year Treasury yield can be found at www.multpl.com/10-year-treasury-rate/table/by-month.

|

Let AAII

Guide Your Investment Future

|

|

AAII

is a nonprofit association dedicated to investment education.

For full access to our award-winning content, classrooms, model portfolios and stock screens, please take a moment to join AAII today for only $29 — a 40% savings off our regular rate. |

Here’s

an example of how the formula works using a target allocation for stocks of

50%. As of early April 2018, the CAPE avg was 22.04, the CAPE20 was 34.29, the

S&P 500 dividend yield was an estimated 1.95% and the 10-year Treasury note

yield was 2.86%. Using whole numbers to represent the target allocation,

dividend yield and bond yield, the stock allocation formula would be:

= [50 + (2 × 22.04) – (2 × 34.29)] × (1.5 × (1.95% ÷ 2.86%)

= [50 + (44.08 – 68.58)] × (1.5 × 0.682)

= 25.5 × 1.023

= 26.09

= [50 + (44.08 – 68.58)] × (1.5 × 0.682)

= 25.5 × 1.023

= 26.09

This reflects

a 26% target allocation to stocks.

The

formula can result in values above 100% and below 0% (meaning negative values).

If the result is greater than 100%, then 100% is used. If the result is

negative, then 0% is used.

Comparison of

Results

In order

to compare the results of the conventional method to the quantitative method,

we need to first establish a model portfolio. The rules governing this model

portfolio are as follows:

1.

The portfolio

is rebalanced once per year.

2.

The stock

portion of the portfolio achieves the same return as the S&P 500, including

dividends. Dividends are not reinvested in stocks but are deposited into the

bonds/cash portion of the portfolio.

3.

The bond and

cash portion of the portfolio collectively achieves a return equal to 80% of

the 10-year Treasury note yield. This is considered to be a conservative

estimate.

Using

the above model portfolio as a basis, over the time period of 1950 through 2017

the quantitative method not only increases the average return of a portfolio

compared to the conventional method in almost every case, but the quantitative

method also reduces the volatility of the portfolio in every case studied (as

measured in the number of years with a negative portfolio return) when compared

to the conventional method.

The

benefits of increased returns to an investor are obvious. The benefits of

reduced volatility, in this case a significant reduction in the number of years

with a negative portfolio return, are more psychological. Even in years where

both models have a negative return, the losses are reduced with the

quantitative method. As an example, in 2008, an investor with a target

allocation of 70% stocks and 30% bonds/cash would have experienced a loss of

23.4% with the conventional method. That same investor would have experienced a

loss of 16.3% using the quantitative method.

{kind=link}

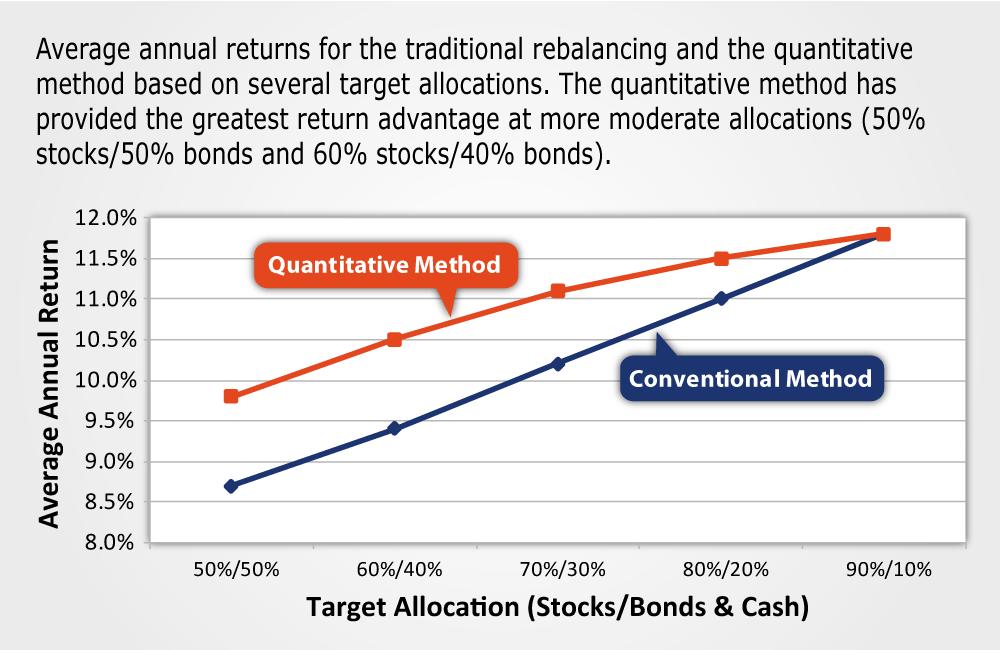

Figure

3 shows a

comparison of average annual returns between the two methods over the time

period of 1950 through 2017, depending on the investor’s target allocation to

stocks and bonds/cash.

Figure

4 shows a

comparison of the number of years with a negative return between the two

methods over the same time period, once again depending on the investor’s

target allocation to stocks and bonds/cash. Both charts are based on

calendar-year holding periods.

As can be seen in Figure

3, the quantitative method provides a distinct advantage in

returns (approximately 1% annually) for target allocations of 50%/50%, 60%/40%

and 70%/30% stocks to bonds/cash. The advantage in returns is reduced for an

80%/20% allocation. The return advantage disappears for a 90%/10% target

allocation.

{kind=link}

Figure

4, on the other hand, shows that the quantitative method reduces

the volatility of the portfolio irrespective of the target allocation, although

the effect is reduced somewhat for higher stock target allocations.

It should be pointed out that both Figures

3 and 4 are based on an investor

rebalancing on the first trading day of October each year. This seems to be the

ideal day to rebalance compared to the first trading day of any other month. On the other

hand, the first trading day of May or June seems to be the least favorable.

However, the quantitative method still provides an advantage in returns for

lower stock allocations (i.e., 50%/50%, 60%/40% and 70%/30% stocks to

bonds/cash) no matter when rebalancing takes place. The advantage in returns

for higher stock allocations (80%/20% and 90%/10% stocks to bonds/cash) can

disappear depending on the time of rebalancing. However, the advantage of the

quantitative method in reducing the volatility of the portfolio is not

significantly affected by the rebalancing date for any target allocation.

Let’s

look at another scenario. What if an investor were able to achieve higher

returns on the bonds/cash portion of their portfolio (e.g., by holding

higher-yielding bonds), for example 120% of the 10-year Treasury note yield? As

expected, the average annual returns are increased for both the conventional

and quantitative methods, but the annual returns are increased by a wider

margin for the quantitative method. The difference in annual returns between

the two methods increases from 0.3% to 0.6%, depending on the investor’s target

allocation. In this scenario, the quantitative method continues to provide significantly

reduced volatility compared to the conventional method.

The Test of

Time

Figure

3 shows

average annual returns for the quantitative method compared to the

conventional method over a time period of 68 years (1950 to 2017). Is it

possible that the quantitative method was only better than the conventional

method for a brief period of time during that period? For example, did it

outperform in the 1950s but hasn’t offered a significant advantage since then?

My

analysis shows that irrespective of the target allocation to stocks, the

quantitative method provided superior returns compared to the conventional

method in the 1950s, 1960s, 1970s, 2000s and so far in the 2010s (i.e., 2010 to

2017).

The

quantitative method slightly underperformed the conventional method in the

1980s, and significantly underperformed in the 1990s. This result makes logical

sense.

The

1990s were famously dubbed as the era of “irrational exuberance” by Alan

Greenspan, who was chairman of the Federal Reserve Board during that period.

Dot-com stocks had extremely high valuations during this period, with a

resulting high value of CAPE20 for the S&P 500. Therefore, the quantitative

model was suggesting a lower allocation to stocks during that period. However,

stocks kept going up anyway, until they didn’t!

The next

decade of 2000 to 2009 was a dismal period for stock returns, with two major

stock market declines. In this decade, an investor with a target allocation of

90%/10% stocks to bonds/cash, using the conventional method, would have

experienced an overall portfolio loss of 1% over the entire 10-year period.

That same investor would have experienced a gain of 44% if the quantitative

method was used. Although 44% is not a great portfolio return for a 10-year

period, it sure beats a loss!

|

TAKE A PEEK

at all the member benefits AAII has to offer. AAII is a nonprofit association dedicated to investment education. |

|

If an investor rebalanced at the time that these

calculations were run in early April 2018, the model would have suggested a

below-target allocation to stocks and an above-target allocation to bonds and

cash.

|

|

|

Target

Allocation

|

Suggested

Allocation

|

|

50% Stocks/50% Bonds and Cash

|

26% Stocks/74% Bonds and Cash

|

|

60% Stocks/40% Bonds and Cash

|

36% Stocks/64% Bonds and Cash

|

|

70% Stocks/30% Bonds and Cash

|

47% Stocks/53% Bonds and Cash

|

|

80% Stocks/20% Bonds and Cash

|

57% Stocks/43% Bonds and Cash

|

|

90% Stocks/10% Bonds and Cash

|

67% Stocks/33% Bonds and Cash

|

What the Model

Currently Says

As of early April 2018, the quantitative model calculates a

current CAPE20 of 34.3, with an average CAPE20 over the last 50 years of 22.0.

Therefore, the model is suggesting a below-target allocation to stocks at the

time the calculations were run. The suggested allocations can be seen in Table

1.

Looking to the

Future

Although

the quantitative method of determining asset allocation that I have described

here has been shown to provide advantages over the conventional method, it is

likely that further improvements could be made to the formula presented in this

article. Such improvements will be the aim of future research in this area.

No comments:

Post a Comment