Succinct Summation of Week’s Events 8.21.15

by Barry Ritholtz -

August 21st, 2015, 4:30pm

Succinct

Summations for the week ending August 21st

Positives:

1.

Housing starts came in at 1.21mm, up from 1.2 and better than the 1.185

expected.

2. Philly Fed came in at 8.3, up from 5.7 and better than the 6 expected.

3. Mortgage rates fell to another multi month low at 4.11%,

4. Refinance applications rose 7.2% and are up 21.2% y/o/y.

5. Japanese exports rose 7.6% y/o/y.

2. Philly Fed came in at 8.3, up from 5.7 and better than the 6 expected.

3. Mortgage rates fell to another multi month low at 4.11%,

4. Refinance applications rose 7.2% and are up 21.2% y/o/y.

5. Japanese exports rose 7.6% y/o/y.

Negatives:

1.

Rough week for stocks, with the S&P 500 posting its largest 5-day decline

since November 2011.

2. FOMC minutes from July reflect a divided committee leaning towards an increase this year, in September or December.

3. Not a whiff of inflation, CPI and core CPI rose just 0.1%.

4. Markit US manufacturing fell to 52.9, the lowest reading since October 2013.

5. Empire manufacturing fell to -14.9 vs expectations of +3.9.

2. FOMC minutes from July reflect a divided committee leaning towards an increase this year, in September or December.

3. Not a whiff of inflation, CPI and core CPI rose just 0.1%.

4. Markit US manufacturing fell to 52.9, the lowest reading since October 2013.

5. Empire manufacturing fell to -14.9 vs expectations of +3.9.

Is

the Bull Market Over?

AUG 21, 2015 11:27 AM

EDT

Is the bull

market, which started after the lows of early 2009, coming to an end? Let's

have a look at some data, as well as the arguments pro and con, to see if we

can find any insight. In particular, I want to look at the latest economic,

corporate and market issues to see what we might learn.

First, the U.S.

economy. As we have observed, it has been a long slog out of the depths of the

financial crisis. Gross domestic product growth has never really taken off; wage

growth is weak; and retail sales, except where cheap credit flows freely, have

disappointed. Many people have little or negative equity in their homes. I have

explained -- or if you prefer, rationalized -- that this is typical of other

post-credit-crisis recoveries.

The primary

upside to the U.S. economy has been job creation, housing and demand for

capital.

Start with the

recovery in the labor market. Unemployment now is 5.3 percent, almost half of

what it was in the aftermath of the crisis; 11 million jobs have been created

since the Great Recession ended. Job openings continue to increase, and there

are signs that wages may finally begin to move higher. This is significantly

better than it has been at any time since 2007.

Second, housing

has improved. It is still below where it should be under normal circumstances,

but as we have noted, these are not normal circumstances. Aided by low

inventory (courtesy of the aforementioned equity issues) and cheap mortgage

rates (courtesy of the Federal Reserve), prices are rebounding. We are also

seeing building permits rise, and bidding wars for both buyers and renters are

not uncommon. In select coastal and urban areas, there are definite supply

shortages. Despite this lumpy and unevenly distributed improvement, the housing

recovery is occurring.

Last, and

perhaps most meaningful for where we are in the current cycle, is demand for

capital. With rates as low as they are, demand for private equity, venture

capital and corporate borrowing has been robust. It has reached the point where

the Fed is thought to be on the verge of raising rates.

One caveat:

U.S. corporations do have a problem deciding what they should do with all their

excess cash. Although the default setting has been share buybacks or dividend

increases, it would be better if they increased research and development and

capital expenditures. That would help drive the next phase of any virtuous

economic cycle.

In general,

profits continue to hang in there. But commodities have been punished, with the

energy sector getting hit hardest; oil is down almost 60 percent from last

year's highs. Lower energy costs typically result in higher consumer (and to a

lesser degree, corporate) spending. That has yet to really show up in the

data.

A similar risk

to corporate profit margins is the competition for workers. It isn't a

coincidence that as unemployment has fallen, low wage shops such as Wal-Mart

and McDonald's have said they will raise wages. At some point in the future,

this should work to the benefit of retail sales, which in turn, lets these

retailers hire more workers and pay them better. Don’t get too excited, as we

have not yet seen much evidence of this particular virtuous cycle.

There are many

negatives, or course -- there always are. But I see two that in particular are

noteworthy. And perhaps surprisingly, the possibility of a Fed rate increase

sometime in 2015 isn't one of them.

The first huge

risk has to be China, which last week joined the currency wars in a sign of

desperation as its economy tanks. Its stock market bubble has popped and it's

dealing with a huge debt overhang. China both reflects and drives a significant

percentage of global economic activity. It looms large when we consider what it

means when industrial metals such as copper and iron ore have huge price

declines. Countries and companies that prospered by feeding China's factories

face the biggest potential hits.

The second

negative has to be the technical deterioration of the markets. I don't trade

day to day, so I am not all that concerned about every 5 percent or 10 percent

pullback. Still, investors who are long never benefit when bull markets

narrowing as this one has. Almost 30 percent of the Standard & Poor's 500

Index components are down 20 percent or more from 52-week highs.

So is the bull

market over?

I find it hard

to reach that conclusion. At the very least, we have been long overdue for a

simple 10 percent correction. And while the economic data has been on the mixed

side, we don’t see the usual indicators of recession, at least in the

U.S.

For individual

stocks, you can certainly tighten up those stop losses. But until we see more

negative economic and corporate data, the option of giving the market the

benefit of the doubt remains the most appealing choice for asset allocation

portfolios.

This column does not necessarily reflect the

opinion of the editorial board or Bloomberg LP and its owners.

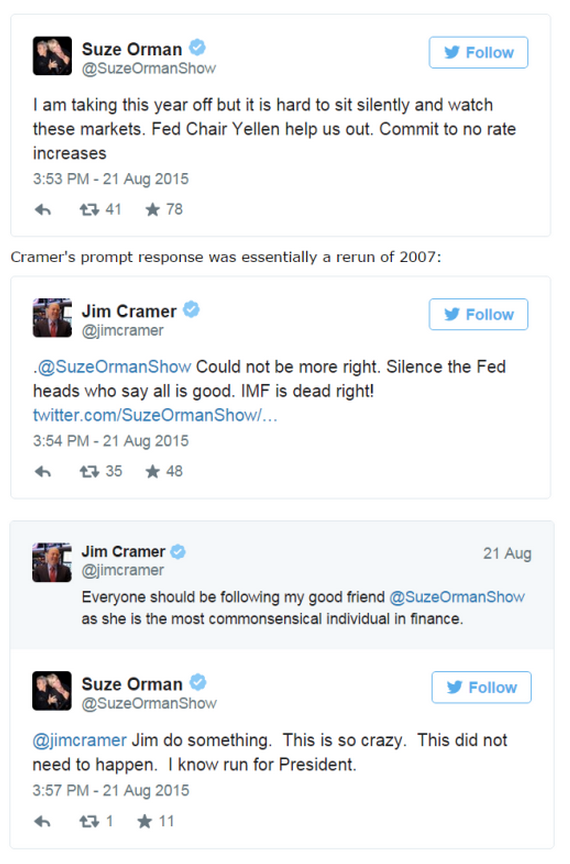

“Demands for

low rates begin as the financial class panics”

No comments:

Post a Comment