Positive:

1) After a wicked sell off, markets recover nearly all of their losses for the past week, now up slightly (tho still below mid-august levels).2) 2Q real GDP growth was revised upwards to 3.7% (Q/Q SAAR) in the second release, a substantial improvement over 3.2% previously.3) Odds of a Fed rate increase fell somewhat in light of China-induced market turmoil.4) Continued recovery in housing: Pending home sales added 0.5% M/M in July;

New home sales added 5.4% M/M in July, increasing to 507,000.5) Core capital goods orders increased 2.2% mom, and core capital goods shipments increased 0.6% mom in July. .6) Conference Board Consumer Confidence Index jumped up to 101.5 in August from 91.0 in July (NOTE: This was Pre-market turmoil)

Negative:

1) China’s economy slows, reflecting the both the law of big numbersa nd a limitation on centrally planned economies.2) China’s stock bubble deflates, after being up as much as 67% YTD, its now negative on the year.3) Crude Oil falls below $40m, then recovers – the most in two days since 2009 — to rebound above $40;4) Personal spending in USA was reported at 0.3% mom in July, below expectations. Core PCE added 1.2% yoy in July.5) University of Michigan Sentiment Index declined to 91.9 in the final report for August from 92.9 in the preliminary report, softer than expected.6) Home prices disappoint, even though annual price appreciation accelerated to 4.5% Y/Y in June, it was still below consensus.7) Although the data on core capital goods orders and shipments were notably stronger than expected, inventories were disappointing, leaving 3Q GDP tracking unchanged.8) Claims in line: Initial jobless claims were reported at 271,000 for the week ending August 22, down slightly from 277,000 in the prior week

What If They Threw a Panic and No One Came? | The Big Picture

“Its enough to give a long-term investor some hope for the future of finance.”

Here’s a bit of role

reversal for you: Mom and Pop were content to ride out the market’s volatility

this past month, more or less sitting tight. Meanwhile, the pros were driven to

the point of near panic.

What was all the fuss

about? Take your pick. Perhaps the China slowdown will cause a global recession.

Maybe the Federal Reserve is going to raise rates and kill the bull market. Oil

prices might fall too far, destroying emerging markets. Or the U.S. economy is

about to go belly-up.

Whatever the fear was,

someone was there to give it voice. The downside of the Twitter era is that

everyone has a megaphone,

and any lack of wisdom of insight is no a deterrent to broadcasting it. This

month, that described Wall Street and not Main Street. It was the pros who lost

it.

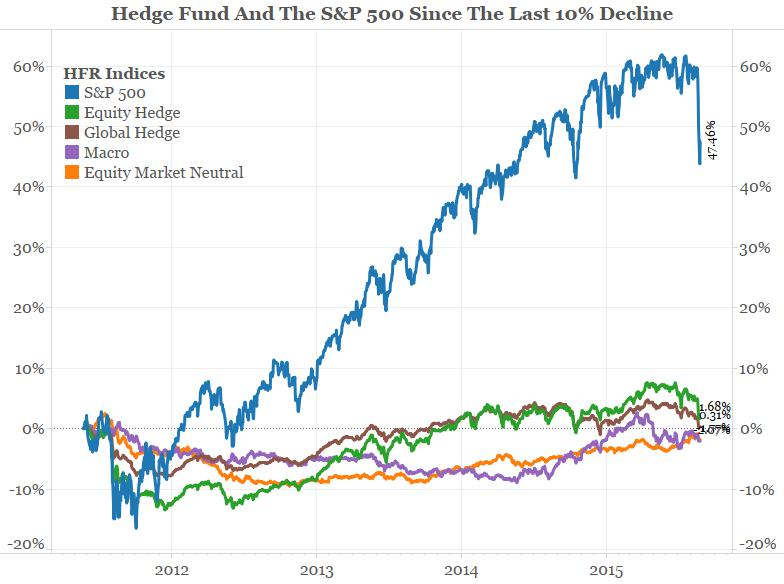

Start with hedge funds.

After missing a generational rally in which the Standard & Poor’s 500 Index

tripled, hedge funds finally began going long U.S. equities — just before the

China trap door swung open. TheWall

Street Journal reported that many funds got shellacked this month, giving up

all of their year-to-date gains in a week. Bridgewater, Omega, Third Point and

Pershing Square all took a beating, but only Omega seemed to be positioned to

capture the bounce-back rally (note that I am not objective, as you can hear

in my

Masters in Business podcast with Omega founder Leon Cooperman).

Beyond the hedge funds, the algorithmic traders

seemed to have run amok as well. It is a natural human response, to borrow from

Daniel Kahneman’s book “Thinking,

Fast and Slow,” to react emotionally first and logically second. However, no

one can think faster than a machine, and the algos managed to engage in some

very fast, and what looked like emotionally driven trading. As we saw this week,

that sort of behavior was amply punished. My colleague Josh Brown summed it up

in a post, “Computers

are the new Dumb Money . . .

You want the box score on this latest weekly battle in the stock market?No problem: Humans 1, Machines 0Because if you think it was human beings executing sales of Starbucks (SBUX) down 22% on Monday’s open, you’re dreaming. And if you believe that it was thinking, sentient people blowing out of Vanguard’s Dividend Appreciation ETF (VIG) at a one-day loss of 26% at 9:30 am, you’ve got another thing coming.

Sometimes

instantaneous is too fast; occasionally the best thing to do is absolutely

nothing. As Gillian Tett of the Financial

Times noted, computers have come to

dominate the trading volume of stock exchanges:

Orders are being executed at lightning speeds in huge volumes. But there is another, often overlooked implication: these machines are being programmed to link numerous market segments together into trading strategies. So when computer programs cannot buy or sell assets in one segment of the market, they will rush into another, hunting for liquidity.

All

this is part of a long series of adaptations by Main Street investors to the

newest new thing, and the countermoves by the (alleged) pros. In response to

this, Mom and Pop have wised up: they trade

lessand invest more. They are tuning out more of the

noise, sending CNBC ratings to record

lows. They are eschewing stock

pickers, and embracing index and exchange-traded funds. They have figured

out that the way you beat high-frequency trading is with low-frequency

investing.

Speaking

of which, the new dumb money got scalded by ETFs. Although U.S. equities as a

whole never fell more than 6 percent, there were widely held ETFs that

temporarily lost one

third of their value.

Ben

Carlson described this as the ETF flash

crash:

In the early minutes of the stock market open on Monday morning things got a little crazy. After a huge whoosh down in overnight futures trading, the NASDAQ fell almost 9% while the S&P 500 was down around 6% right after the opening bell. Watching it in real time was a sight to behold. Less than 15 minutes later, a huge chunk of those losses were recovered. Many individual stocks saw even larger moves.

Mom

and Pop outwitting high-frequency traders; hedge funds being beaten by Main

Street. It's enough to give a long-term investor some hope for the future of

finance.

This column does not necessarily reflect the opinion

of the editorial board or Bloomberg LP and its owners.

No comments:

Post a Comment