|

By Dave Moenning on Feb 11, 2019 07:25 am

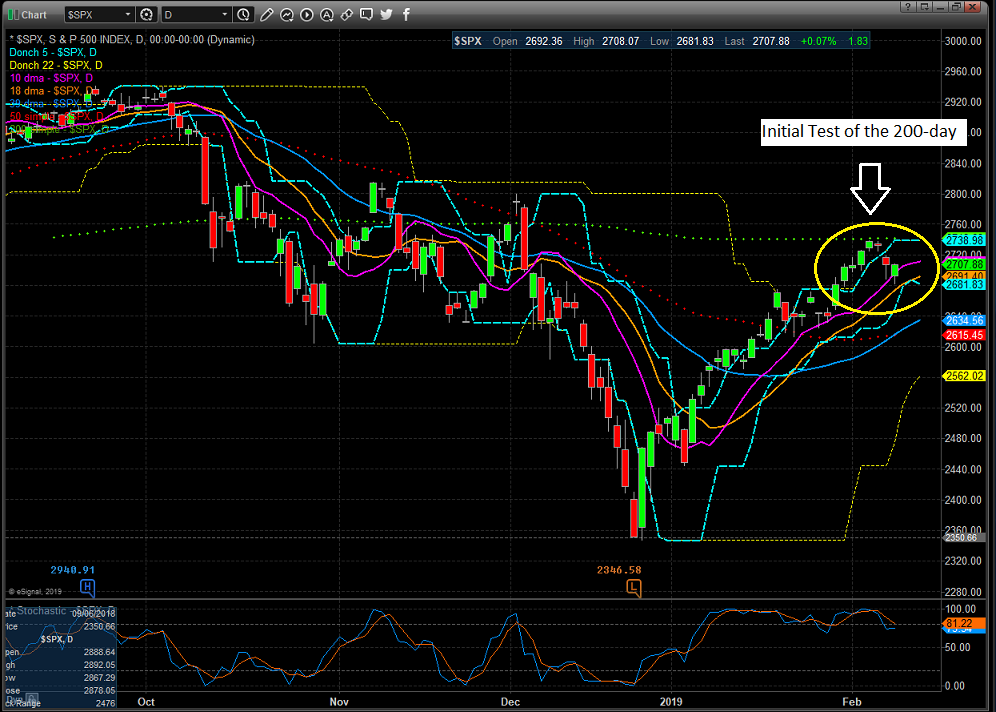

On Tuesday, February 5 and again on Wednesday, February 6,

the S&P 500 bumped into its 200-day moving average. While I'm not

exactly sure why this particular indicator captures the attention of so

many (there are a myriad of more effective trend-following tools readily

available), the crossing of the 200-day is viewed as a big deal. Some go so

far as to say the moving average represents a line in the sand between the

bulls and the bears. As in, if the current price of a security or index

resides above its 200-day, it is considered a bull market and if below, a

bear market.

Personally, I don't subscribe to such a view. However, it is

worth noting that a great many investors, including throngs that get paid

to invest other people's money, do see the 200-day as a critical line of

demarcation. Thus, how the market acts when it approaches its 200-day is

viewed as important.

So, what was the market's reaction when the S&P 500

"tested" its 200-day for the first time in 42 days? See for

yourself...

While I wouldn't call it an abject failure, the index did

pull back a bit after flirting with the all-important line in the sand for

a couple days. So, the question, of course is what, if any message should

we take from the initial "bonk" at the 200-day?

The Bull's View

Always optimistic, those wearing their bull caps last week

viewed the action as positive. The words "a pause that refreshes"

were bandied about quite a bit in the bull camp. After all, even the most

ardent bull will admit that stocks have run a long way in a short period of

time, that the indices are overbought, and that sentiment has rebounded

quite a bit. As such, a brief respite before the real run for the border

begins certainly makes sense.

I'll add that last week's intraday action was pretty darn

good. With stocks overbought and bumping into resistance, the bears could

have easily grabbed control of the game and proceed scare the bejeebers out

of everyone again based on some of the headlines.

If you will recall, there was the declaration that Trump

wasn't planning on meeting with China's Xi Jingping before the March 1

tariff deadline (initial positioning?). There were some not-so-hot economic

data. And there was word that global growth appears to be slowing more than

expected.

It Isn't The News, It's...

But as the saying goes, it isn't the news, it's how the

market reacts to the news that is important. And yes, stocks did fall on

Thursday and opened lower again on Friday. But given that the market

rallied fairly vigorously off the lows on both days, one has to be

impressed that the bulls were not run over and actually held their ground

rather nicely.

Tape readers tell us that this was "good action"

and therefore, we should expect further rally attempts in the coming days.

Backing up their claim from a fundamental perspective, our

heroes in horns contend that the current rally reflects a

"correction" of December's fear-based selling. The Fed changed

its course and promised not to be stubborn. And then on the trade front,

everybody expects a deal of some form to get done sooner rather than later.

And since the President is known for negotiating via his Twitter account,

last week's developments could be ignored.

So, with two of the big three fears out of the way and the

current earnings parade being viewed as "not as bad as feared,"

the bulls argue that it's onward and upward from here.

The Bear's View

As you might suspect, our furry friends have a slightly

different take here. Those in the bear camp remind us that a robust bounce

off an emotional low is completely normal and that more times than not, the

indices tend to revisit or "test" the lows a time or two. Thus,

the failure to simply blast through the 200-day suggests that the recent

bounce may have run its course.

Those seeing the market's glass as half-empty counter the

"good action" argument with the idea that "FOMO" (fear

of missing out) and a dip-buying mentality has returned, and that neither

is likely to last long.

The reasoning here is the market's third big fear

(#GrowthSlowing) has not been "solved." In fact, the problem is

getting worse.

Bond Yields Not Jiving

Exhibit A in the bear camp's argument is the action in the

bond market. In short, yields all over the globe are falling. And the U.S.

is not exempt as the 10-Year made a new 13-month/cycle low last week.

As the chart above illustrates, the yield on the U.S.

10-Year has fallen from above 3.2% in November to 2.6% last week. Not

exactly the type of behavior one might expect during a stock market rally.

Looking around the globe, the trend is the same. The yield

on the German Bund has declined to 0.09%, from above 0.50% in October. And

Japan's 10-Year yield went negative.

On that note, according to Bloomberg, nearly $9 trillion of

global bonds ended the week with negative yields, an amount that is up

about 50% since late last year.

The key point is that falling rates don't jive with an

"everything is peachy keen" stock market outlook. So, while the

stock market appears to be in an optimistic mood, bond traders have a

different view.

The problem here is pretty straightforward - global growth

continues to slow. For example, the European Commission cut its 2019 GDP

estimate by nearly a third last week. The expectation for eurozone GDP

growth now stands at 1.3%, down from 1.9%. That was a hefty cut, and a

surprise to many.

Next, Italy wins the booby prize for being the first country

to officially enter recession. Growth in Germany is faltering due to the

slowdown in China. Australia's central bank cut it's outlook for the

country's growth. And India's central bank surprised traders by cutting

rates last week.

And yet, investors here at home seem to think that the U.S.

will be immune to slowing global growth. Hmmm...

Maybe The Fed Caved Because...

At the very least, we may want to consider that Powell's

bunch didn't cave to either political or market pressure. No, perhaps the

Fed's new "patient" stance is tied to door number three:

#GrowthSlowing.

Yes, it is indeed positive that the Fed has said it won't

accidentally drag the U.S. into recession by going too far with their rate

hikes. And it is also positive that everybody expects a deal to get done

with China. From my seat, the argument can be made that ending the trade

spat could possibly mark an end to the #GrowthSlowing movement and

reinvigorate global economic growth.

Which brings us back to the question at hand. Will stocks

break above the 200-day and send an all-clear signal to bullish investors

near and far? Or have the bulls used up their lot of good news in getting

back to the 200-day?

Time will tell, of course. But, I for one, am going to

continue to watch the action in the bond market as a "tell" on

the issue of global growth.

|

{kind=link}

{kind=link}

No comments:

Post a Comment